Blog + News

Our Review of the 2023 Federal Budget

On March 28, 2023 (“Budget Day”), the Honourable Chrystia Freeland delivered the 2023 Federal Budget (the “Budget”). While our Budget summary focuses exclusively on taxation topics relevant to our clients and friends, it’s worth noting that the Budget proposes a $40B+ deficit for the coming year with no plan to bring Canada’s finances back into balance. When questioned on this, the Finance Minister’s answer came across as being unconcerned. Well, suffice it to say that our Firm is concerned; and every Canadian should be given the high and ever increasing debt loads, rising interest rates and inflationary environment that our country is currently facing. With every increasing dollar that goes to service debt financing costs, that is one less dollar that must be taken away that could provide future essential government services, additional tax revenues that need to be raised, a reduction of future services or a combination of all. Not great. It would have been good to at least see a plan towards budgetary balance.

Every year, prior to the delivery, prognosticators predict what tax measures the Budget might contain. Our firm did this via our Budget predictions podcast (which can be listened to here) and overall, surprisingly, we were somewhat accurate. There were some surprises, though, as we’ll explain further below.

A. EXECUTIVE SUMMARY

First, let’s quickly summarize what is NOT included in the Budget:

- No personal tax rate increases. There were some rumblings immediately prior to the Budget that the Government would introduce more “tax the rich” measures such as increased personal tax rates for the so-called “wealthy” or super-high income earners. No such measures – other than amendments to the alternative minimum tax – are contained in the Budget as we predicted.

- No corporate tax rate increases. Like the above, some were predicting that corporate tax rates would increase especially given the government’s rhetoric that it likes to trumpet (including in this Budget) that the government will not engage in a “race to the bottom” for corporate tax rates. Thankfully, as we predicted, the Budget did not contain such measures.

- No increase in the capital gains inclusion rate. Every year, almost without exception, there are a large number of prognosticators who predict the capital gains inclusion rate would increase. We have always not agreed with those predictions except for the last couple of years. We predicted there would not be an increase to the inclusion rate this year (since we believe the time for such an increase has passed) and thankfully we were correct.

- Despite the calls of many from the tax community for over a decade, no introduction of comprehensive tax review / reform. We accurately predicted this, but our firm was surprised by the introduction by the Province of Ontario of a comprehensive tax review when it announced its Budget last week (not many details are available). It is long overdue for the federal government to undergo comprehensive tax review / reform.

- No introduction of a “wealth tax”. The fury over this topic has died down over the last year or so and the Budget contains no such measures to introduce a wealth tax.

- While the Budget does contain significant changes to the existing inter-generational transfer rules under Bill C-208, there are no further proposed changes to curb “surplus stripping” type of transactions.

- No change to the paragraph 55(5)(e)(i) butterfly exception for siblings introduced by Bill C-208.

Here is a quick list of proposed changes that ARE included in the 2023 Budget:

- Changes to the Inter-generational transfer rules introduced in Bill C-208. The government has long promised changes to the very deficient rules in Bill C-208 and the Budget now contains those proposals.

- Introduction of legislative proposals to introduce employee ownership trusts as had been promised by the Government.

- Changes to the existing alternative minimum tax (“AMT”) regime.

- Significant changes to the general anti-avoidance rule (“GAAR”).

- Introduction of automatic tax filing by the Canada Revenue Agency (“CRA”).

- Changes to the retirement compensation arrangement (“RCA”) rules.

- Changes to registered disability savings plans (“RDSPs”).

- Updates to the Implementation of OECD BEPS Pillar Two – Global Minimum Tax.

- Changes to Registered Education Savings Plans (“RESPs”)

- Introduction of additional GST tax credits for lower income Canadians via the so-called “Grocery Rebate”.

- A whole host of “green” incentives and tax credits. Our blog will purposely ignore these incentives and credits.

B. RELEVANT BUDGET DETAILS

1. Changes to the Inter-Generational Transfer Rules Contained in Existing Bill C-208

The section 84.1 amendments introduced by a private member’s bill (Bill C-208) became law effective June 29, 2021. Those 2021 amendments were aimed at exempting from the application of section 84.1 (which can convert an otherwise taxable capital gain into a taxable dividend in specific situations as further explained below) certain share transfers from parents to corporations owned by their children or grandchildren. It was widely recognized that few restrictions were placed around these rules, in particular with respect to whether the business was ‘genuinely’ being transitioned to the next generation. Because an inter-generational business transfer is a multi-faceted matter that involves family dynamics and frequently a gradual transition of ownership and management, it was a real challenge for the Department of Finance (“Finance”) to put together conditions or hallmarks that would test for an actual business succession scenario (while taking into account the unique aspects of an inter-generational business transfer) while ensuring that the door is not opened too far so as to encourage abusive tax avoidance. The proposed amendments to section 84.1 contained in Budget 2023 is Finance’s attempt at doing so, and if enacted the amended rules would apply to a disposition of shares that occur on or after January 1, 2024.

First, what is section 84.1? Section 84.1 of the Income Tax Act (the “Act”) applies when an individual or trust (the “Vendor”) disposes of shares of a Canadian-resident corporation (the “Subject Corporation”) to another corporation (the “Purchaser Corporation”) with which the Vendor does not deal at arm’s length, and immediately after the disposition, the Subject Corporation is “connected” with the Purchaser Corporation. Generally speaking, a Subject Corporation would be connected to the Purchaser Corporation if after the disposition the Purchaser Corporation owns more 10% of the Subject Corporation, or it – together with other non-arm’s length persons – owns more than 50% of the voting shares of the Subject Corporation. If applicable, section 84.1 will convert the otherwise capital gain that would have been recognized on the transfer to a taxable dividend. This has a two-fold impact. First, taxable dividends are usually (depending on the marginal tax bracket of the Vendor) taxed higher than capital gains (which have a 50% inclusion rate). Second, such a conversion to taxable dividends disqualifies the Vendor from utilizing his / her available capital gains deduction since such a deduction is not available to be utilized against taxable dividends. Ouch! Since many inter-generational transfers would cause the application of section 84.1 to apply, many in the tax community have long been calling for this inequity to be fixed. This inequity has existed since the introduction of the capital gains deduction in 1985 so the government has been very slow to respond to this issue. However, the enactment of Bill C-208 in 2021 forced the issue and thus the amendments that now appear in Budget 2023.

The Bill C-208 amendments enacted in June 29, 2021, provided an exception from the application of section 84.1 by deeming the Vendor to be dealing at arm’s length with the Purchaser Corporation where the Vendor disposed of qualified small business corporation (“QSBC”) shares or shares of the capital stock of a family farm or fishing corporation (“QFFP”) to a Purchaser Corporation that was controlled by an adult child or grandchild or the Vendor, and certain other conditions were met.

The Budget 2023 proposed amendments will still require that these essential elements, i.e. the Vendor must still be a natural person and what is being sold must still be QSBC shares or QFFP shares. However, the other conditions are being replaced wholesale, namely there would no longer be:

- A requirement that shares of the Subject Corporation not be disposed of by the Purchaser Corporation within 60 months [existing paragraph 84.1(2.3)(a)];

- A purported reduction to the availability of lifetime capital gain exemption where the Subject Corporation’s taxable capital exceeds certain threshold [existing paragraph 84.1(2.3)(b)]; and

- A requirement to obtain an independent assessment of the fair market value of the subject shares and a third party affidavit attesting to the disposal of shares [existing 84.1(2.3)(c)].

Instead, the parties involved in the inter-generational business transition must meet one of two proposed transfer options:

- An Immediate Intergenerational Business Transfer, or

- A Gradual Intergenerational Business Transfer.

Where the requirements are met, section 84.1 will not apply to the disposition of the shares by the Vendor. Also, the proposed rules will provide for a new ten-year capital gains reserve rather than the usual five-year capital gain reserve.

Further, the next generation to which the business can be transferred has been expanded from just children and grandchildren. According to the proposed amendments, a “child” will also include the expanded meaning of a child in existing subsection 70(10) of the Act as well as a niece/nephew, a niece/nephew of the Vendor’s spouse or common-law partner, or a spouse, common-law partner (“CLP”) or child of such person.

Note that where there is a trust involved in the structure, the proposed rule contains a deeming rule in proposed 84.1(2.3)(b) whereby, for the purpose of reading these hallmarks above, a beneficiary of a discretionary trust is deemed to own all everything that is owned by the trust.

Immediate Intergenerational Business Transfer

In order to qualify under the “Immediate Intergenerational Business Transfer” option, all of the following conditions from (a) to (h) below must be met:

a) Immediately before the disposition of the subject shares (hereafter referred to as the ‘disposition time’), the Vendor either alone or together with the Vendor’s spouse or CLP, must control the Subject Corporation, and no other person may have de jure or de facto control of the Subject Corporation.

Moodys Tax Commentary:

At first glance, this appears to be strict requirement that requires that the business being transitioned must be currently controlled, legally and factually, by one person (and their spouse or CLP). However, the draft legislation as written does allow for pre-sale planning that will permit a non-controlling owner of a qualifying business to take advantage of these new rules. For instance, a non-controlling shareholder can transfer their shares in a QSBC to a holding corporation (Holdco) that is wholly controlled by that individual under a tax-deferred rollover election under subsection 85(1) of the Act prior to the sale event. Holdco will become the Subject Corporation for that Vendor individual, and as long as the rollover transaction qualifies under paragraph 110.6(14)(f), the shares in Holdco will not be deemed to be owned by an unrelated person for purposes of the 24-month holding period test.

b) At the disposition time, the Vendor must be an individual (other than trust), the Purchaser Corporation must be controlled by one or more adult “children” of the Vendor – meaning of child is expanded for this purpose as described above, and the subject shares must be QSBC or QFFP shares.

c) At all times after the disposition, the Vendor either alone or with a spouse or CLP does not have either de jure or de facto control over

-

- The Subject Corporation;

- The Purchaser Corporation; or

- Any other person or partnership (hereafter referred to as a “relevant group entity”) that carries on, at the disposition time, an active business (hereafter referred to as a “relevant business”) that is relevant to the determination of whether the subject shares satisfy the QSBC or QFFP test.

Moodys Tax commentary:

This requires that the Vendor individual or their spouse/CLP not have any legal and factual control over the business, immediately after the disposition. While it is easy to structure a sale to make sure legal control is removed from the hands of the Vendor, it will often be challenging to substantiate that the Vendor no longer has factual control. It will be prudent for taxpayers taking advantage of these rules to properly document how strategic and daily business decisions are being taken over completely by the next generation (e.g. minutes of board meetings, email correspondences, etc). If the Vendor is still involved, they should merely be acting as consultants and must not have any decision-making powers.

The relevant group entity and relevant business concept appears somewhat confusing. What appears to be the intention here is to ensure that the requirement of control being given up applies to the whole chain of corporate or partnership entities below the Subject Corporation. Let’s use the pre-closing transaction mentioned in our commentary for (a) above as an example. In our example, we have Vendor individual transferring their shares in a QSBC to a Holdco. Since the active nature of the QSBC’s business would be relevant in qualifying the Holdco shares as QSBC shares, the QSBC entity would be a “relevant group entity” and its active business would be a “relevant business”. Therefore, this requirement ensures that the Vendor individual (or their spouse/CLP) cannot retain any legal or factual control over the Holdco as well as over the QSBC.

d) At all times after the disposition time, the Vendor does not – either alone or with a spouse/CLP – own directly or indirectly:

-

- 50% or more of any class of shares, other than shares of a “specified class” as defined in subsection 256(1.1) (hereafter referred to as “non-voting preferred shares”), of the Subject Corporation or of the Purchaser Corporation; or

- 50% or more of any class of equity interest (other than non-voting preferred shares) in any relevant group entity.

Moodys Tax Commentary:

Under the existing Bill C-208 rules, it is not uncommon for parents to sell just enough shares of a QSBC or QFFP to utilize their lifetime capital gain exemption (for QSBC shares, $913,630 for year 2022 but $971,190 for 2023) to the Purchaser Corporation and depending on the value of the QSBC or QFFP, such shares being sold could just account for a minority of the value of the Subject Corporation. This would no longer be allowed under the Immediate Intergenerational Business Transfer Option since the Vendor cannot retain more than 50% of any classes of shares of the Subject Corporation, Purchaser Corporation or any relevant group entity, unless the shares being retained are “specified class” shares.

Generally speaking, specified class shares are non-voting freeze shares that are redeemable for no more than the fair market value of the consideration for which they are issued, and a dividend rate that is limited to the prescribed rate of interest at the time the shares were issued. There are often freeze shares that do not comply with the specified class requirement because although the dividend is limited to a percentage of the redemption amount, that dividend rate is not limited by the prescribed rate at the time the shares were issued. In such situations, these freeze shares would need to be amended to meet the specified class conditions in order for the Vendor to retain these shares after an immediate intergenerational business transfer disposition.

Overall, we understand why Finance wants the Vendor to not have legal control. However, this requirement introduces significant risk to the Vending Parent that a child could run the business into the ground without the ability to influence the direction of the corporation. Careful consideration will need to be given to the Vendor Parent if they want to take advantage of this new proposal.

e) Within 36 months of the disposition time and at all times thereafter, the Vendor (and their spouse/CLP) does not not own, directly or indirectly,

- Any shares, other than “non-voting preferred shares” of the Subject Corporation or of the Purchaser Corporation, or

- Any equity interest (other than “non-voting preferred shares”) in any relevant group entity.

Moodys Tax Commentary:

Note that “non-voting preferred shares” referred to here are shares that meet the “specified class” shares definition as discussed above.

In other words, this is a hard deadline of 36 months, where the Vendor and their spouse/CLP must get rid of all shares of any of the corporations, except for the freeze shares that meet the specified class shares definition.

f) From the disposition time until 36 months after that time:

- The child or group of children legally controls the Subject Corporation and the Purchaser Corporation;

- The Child or at least one member of the group of Children is actively engaged on a regular, continuous and substantial basis (within the meaning of the TOSI rules in paragraph 120.4(1.1)(a) of the Act) in a relevant business of the Subject Corporation or a relevant group entity; and

- Each relevant business of the Subject Corporation and any relevant group entity is carried on as an active business.

Moodys Tax Commentary:

Immediately from the disposition time, the Vendor’s children must have legal control of the Subject Corporation and Purchaser Corporation. Note that this does not require these children to have control over all entities underneath Subject Corporation, so it is possible that the underlying business not be controlled by these children.

At least one Child must meet the regular, continuous and substantial actively engagement test (the TOSI excluded business test), but that only needs to be in respect of at least one of the relevant business. For the remainder of the discussion, we will refer to such Child or Children as the ‘active children’.

Immediately from the disposition time and until 36 months after, all “relevant business” must be carried on as an active business. Recall that a “relevant business” is an active business carried on by each relevant group entity. In other words, in order to meet this condition, the active business carried on by Subject Corporation or by any underlying corporate or partnership subsidiary of the Subject Corporation must not cease and must continue to keep running as an active business throughout the 36-month period subsequent to the disposition time. Presumably this rule is to ensure the business is actually being continued on by the next generation.

g) Within 36 months of the disposition time (or a greater period of time as is reasonable in the circumstances), the Vendor (and their spouse/CLP) takes reasonable steps to:

- Transfer management of each relevant business of the Subject Corporation and any relevant group entity to the active children; and

- Permanently cease to manage any relevant business of the Subject Corporation and any relevant group entity, and

h) The Vendor and all the Children must jointly elect for paragraph 84.1(2)(e) to apply to the disposition and file the election by the Vendor’s filing-due date for the disposition year.

Note that the proposed rules also add a relieving provision to conditions (f) and (g) above. According to proposed subparagraph 84.1(2.3)(c)(i), conditions (f) and (g) will not be considered to fail if the children subsequently sell all of the shares of the Purchaser Corporation, the Subject Corporation and all relevant group entities to an arm’s length purchaser, provided that all equity interests in all relevant businesses are included in the subsequent disposition. Also, per proposed subparagraph 84.1(2.3)(d)(i), if the active child dies or suffers a severe and prolonged impairment in physical or mental function, conditions (f) and (g) are deemed to be met as of the time of the death or mental or physical impairment.

Gradual Intergenerational Business Transfer

To qualify for the Gradual Intergenerational Business Transfer option, all of the conditions in (a) to (i) below must be satisfied. The framework for these conditions are similar to those established for the Immediate Intergenerational Business Transfer option. In fact, conditions (a), (b), (d), (e) are the exact same as conditions (a), (b), (d), (e) of the Immediate Intergenerational Business Transfer option, and the election requirement in condition (i) is the same as the election requirement in condition (h) above.

Below are how the Gradual Intergenerational Business Transfer proposals differ from the Immediate option:

(c) [Similar to condition (c) of the Immediate Intergenerational Business Transfer option, except that the Vendor (or their spouse/CLP) is permitted to retain de facto control immediately after the disposition time: this is a relieving aspect of the gradual option]

At all times after the disposition, the Vendor either alone or with a spouse or CLP does not have de jure control over

- The Subject Corporation;

- The Purchaser Corporation; or

- Any relevant group entity that carries on, at the disposition time, a relevant business.

(F) [This condition is not found in the Immediate Intergenerational Business Transfer option and is the key ‘punishing’ clause for choosing the Gradual Intergenerational Business Transfer option]

Within 10 years after the disposition time and at all times after, the Vendor (or their spouse/CLP) does not own, directly or indirectly:

- Where the subject shares are QFFP shares, interests (including any debt or equity interest) in any of the Subject Corporation, Purchaser Corporation, and any relevant group entity with a fair market value that exceeds 50% of the fair market value of all the interests that were owned, directly or indirectly, by the Vendor (or their spouse/CLP) immediately before the disposition time.

- Where the subject shares are QSBC shares, interests (including any debt or equity interest) in any of the Subject Corporation, Purchaser Corporation, and any relevant group entity with a fair market value that exceeds 30% of the fair market value of all the interests that were owned, directly or indirectly, by the Vendor (or their spouse/CLP) immediately before the disposition time.

The moment within this 10-year period that Vendor reduced their holdings to the 50% or 30% permitted threshold, as the case may be, it is hereafter referred to as the “Final Sale Time”.

(G) [Similar to condition (f) of the Immediate Intergenerational Business Transfer option, except that the 36-month period is extended to the later of 60-months and the Final Sale Time: this is the second punishing aspect of the gradual option]

From the disposition time until the later of 60 months after disposition time and the Final Sale Time:

- The child or group of children legally controls the Subject Corporation and the Purchaser Corporation;

- The Child or at least one member of the group of Children is actively engaged on a regular, continuous and substantial basis (within the meaning of the TOSI rules in paragraph 120.4(1.1)(a) of the Act) in a relevant business of the Subject Corporation or a relevant group entity; and

- Each relevant business of the Subject Corporation and any relevant group entity is carried on as an active business.

Note that the relieving provision for an arm’s length sale, or death or physical/mental impairment of an active child, also applies to this condition (g) of the Gradual Intergenerational Business Transfer also. These proposed rules are contained in subparagraphs 84.1(2.3)(e)(ii) and (d)(ii).

(H) [Similar to condition (g) of the Immediate Intergenerational Business Transfer option, except that 36-months is extended to 60-months: this is a relieving aspect of the gradual option]

Within 60 months of the disposition time (or a greater period of time as is reasonable in the circumstances), the Vendor (and their spouse/CLP) take reasonable steps to:

- Transfer management of each relevant business of the Subject Corporation and any relevant group entity to the active children; and

- Permanently cease to manage any relevant business of the Subject Corporation and any relevant group entity, and

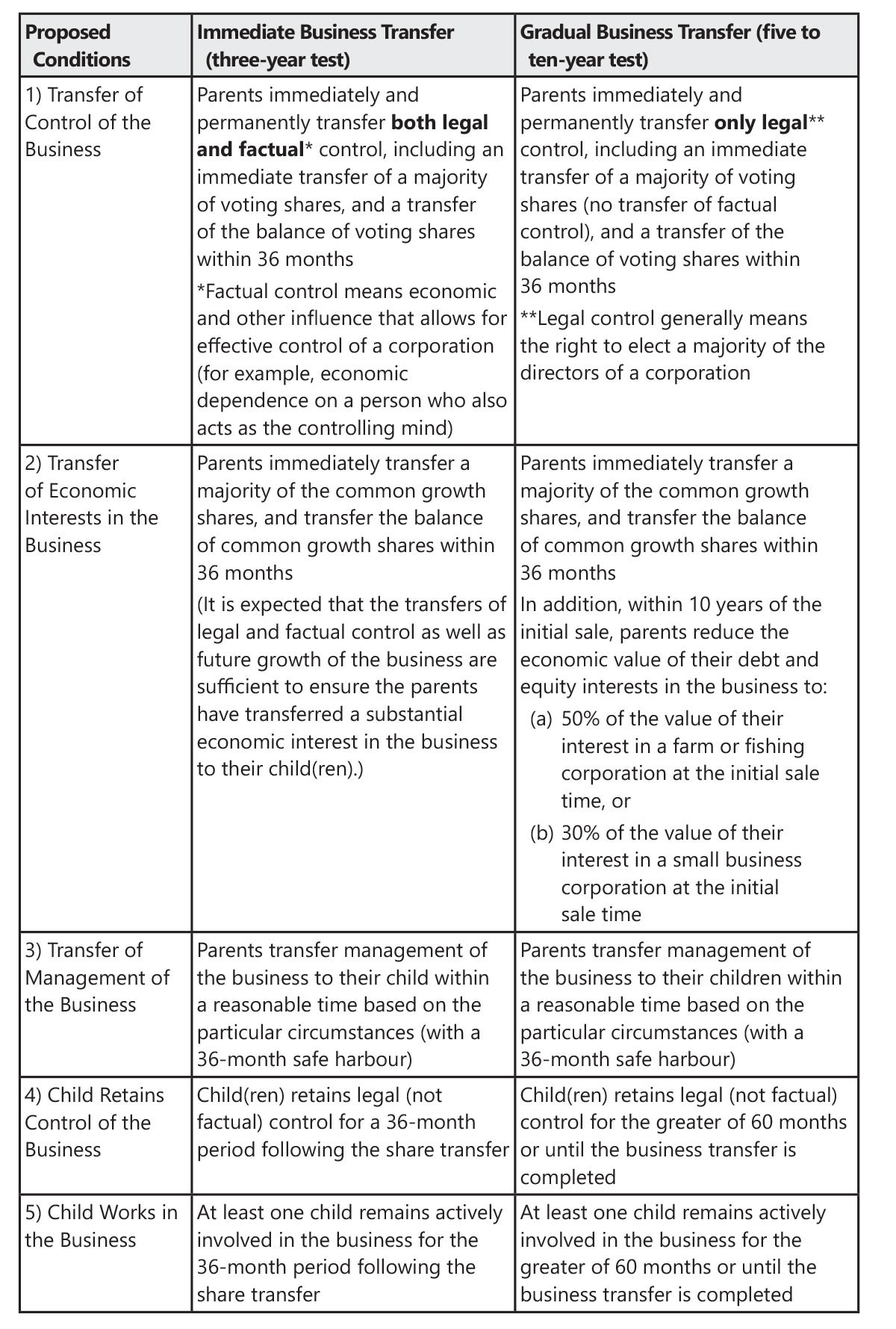

The following summary table provided by Finance in the Budget documents provides a visual summary of the comparison of the requirements of these two options:

When to choose the immediate vs the gradual transfer option?

The Gradual Intergenerational Business Transfer option has the following two obvious advantages over the Immediate option:

- It is not required that the Vendor (along or together with their spouse/CLP) give up de facto control immediately after the disposition time; and

- The Vendor has up to 60 months (rather than 36 months) to take steps to transition management to the active children.

However, the obvious two disadvantages of the Gradual Intergenerational Business Transfer over the Immediate option are:

- Whereas in the Immediate Intergenerational Business Transfer option, the Vendor (or their spouse/CLP) may keep shareholder loan receivables and freeze shares that meet the specified class definition for as long as they want, they must get rid of them down to the 30% or 50% of value threshold (depending on whether the subject shares are QSBC shares or QFFP shares) within 10 years from the disposition time. Depending on the quantum of these shareholder loans and freeze shares, this could cause a cash flow strain on the operating companies as well as cause significant dividend income taxation to the Vendor (or their spouse/CLP); and

- Until the later of 60 months (rather than 36 months) and the Final Sale Time when the 30%/50% threshold is met, all of the active businesses of the group must continue to be carried on as active businesses, at least one of the children must be actively engaged in one of the businesses, and the children must retain legal control.

In most cases, it appears the incentive to make an Immediate Intergenerational Business Transfer work will be significant, and it can sway a business owner’s decision to attempt to completely step down from management just to take advantage of this option.

The child (or children) would be jointly and severally liable for any additional taxes payable by the Vendor, if section 84.1 applies due to the transfer not meeting the requirements discussed. This ensures that the child or children have an interest in properly and actively taking over the business and its management so as to make sure the Vendor in fact meets the required conditions.

To ensure the CRA will have the time to take necessary audit and enforcement actions, the limitation period for reassessing the Vendor’s liability for tax that may arise of such business transfers is proposed to be extended by an three years for an Immediate Intergenerational Business Transfer and by ten years for a Gradual Intergenerational Business Transfer.

2. Employee Ownership Trust

The concept of Employee Ownership Trusts (EOT’s) was first introduced as a discussion point in the 2021 Federal Budget when it was announced that the government would engage with stakeholders to determine the impediments to the creation of these specific trust vehicles in Canada. It was largely held that a well-crafted EOT regime would facilitate increased employee ownership of privately-held businesses and that the timing was right to be able to learn from the U.S. and U.K. experience with respect to these special purpose entities.

Although EOT’s were fist recognized in the US as early as 1897, settled and established law did not create the first EOT until 2015. Similarly, UK law evolved to formally recognize EOT’s in 2014 with over 100 companies becoming employee-owned in 2019 alone.

With our leading trading partners having adopted the EOT model, Budget 2022 committed to the draft legislation provided in Budget 2023 to create the new dedicated type of trust under the provisions of the Act to support employee ownership. The proposed EOT structure will present a succession planning option to owners of privately held corporations to allow employees of the corporation to acquire the corporation’s shares without requiring them to directly pay for the shares.

Certain qualifying conditions must be met in order for a trust to be considered a qualifying EOT:

- The trust must be Canadian resident and must have only two purposes:

- To hold shares of qualifying businesses for the benefit of employee beneficiaries; and,

- Make formula-based distributions to employee beneficiaries.

- The EOT must hold a controlling (more than 50%) interest in in one or more qualifying businesses.

- All or substantially all (90% or more) of the EOT’s assets must be shares of one or more “qualifying businesses”.

- A qualifying business must meet certain conditions:

- All or substantially all (90% or more) of the fair market value of its assets must be used to carry out an active business in Canada; and

- The business cannot be carried out as a partner to a partnership.

- The EOT cannot directly allocate shares of a qualifying business to specific beneficiaries of the EOT.

It is important to consider the qualifying conditions of the underlying business as it is conceivable that a successful business could run afoul of the conditions that must be met over the fullness of time. Firstly, it must be noted that the asset test (90% or more in the form of active business assets) must be met ALL OF THE TIME. Second, as a successful operation can quite easily accumulate excess cash, it will need to justify the purpose of the cash as it relates to maintaining active business pursuits. Building a cash reserve for expansion would potentially cause the business to no longer qualify and attract some rather nasty tax consequences (such as subsection 15(2), discussed later).

The manner in which the EOT is governed is also subject to specific conditions:

- Trustees (including corporate trustees) must be Canadian residents;

- The trustees are elected every five years by the beneficiaries of the EOT; and

- When a business owner sells his business to an EOT, he (or anyone related to him who also had a significant interest in the business) cannot form more than 40% of the Trustees, the Board of Directors of the qualifying business or the Board of Directors of a corporate trustee.

In general terms, the beneficiaries of an EOT are the employees of the qualifying business that have been sold to the EOT. The definition of a “qualifying employee” captures all employees employed directly by the qualifying business as well as all employees of other businesses that it controls. There are some exclusions as well – employees (or persons related to the employee) who were significant shareholders of the qualifying business pre-sale are excluded from being a beneficiary. In addition, if an employee has not been employed for a minimum of 12 months, they will also be excluded as beneficiaries.

Some things to think about or be aware of with respect to employee-beneficiaries:

- What happens in the event a non-resident employee or an employee who is a U.S. citizen must be included as a beneficiary of the Trust? In such case, not only is there withholding tax and related compliance that must be completed by the Trust, but also the employee may have unwanted non-Canadian tax implications (such as cumbersome US reporting for the US citizen beneficiary).

- If an employee passes away or is removed from the payroll because they became disabled, they or their surviving family member can no longer benefit from the Employee Ownership Trust. Is this fair? Finance may wish to consider amendments to create a class of “qualifying former employees”.

- An employee is restricted from additional investment into the business by way of an acquisition of equity from the founder who may have retained a non-controlling share in the business or the EOT itself. If he/she acquires more than 10% of the business, they will be excluded as a beneficiary of the EOT. However, it appears that phantom equity arrangement, options and warrants (again, assuming the 10% threshold of ownership is not breached) can be considered.

How does it work?

When a business owner decides to sell his/her business to an EOT, for the benefit of his / her employees, they will enter into a purchase and sale agreement with the EOT (or a corporation wholly-owned by the EOT). The shares of the qualifying business will be sold for an amount that is not in excess of the fair market value of the business and, as a result of the transaction, the EOT must have either directly, or indirectly, a controlling interest in the qualifying business immediately after the sale.

Typically, the EOT will not have the proceeds available to fully pay the vendor for the purchase of the shares of the qualifying business. This is the primary appeal of the EOT structure – the opportunity for employees to “buy” a company “for free” as it is the EOT that will be required to finance the purchase of the shares through an advance from the corporation itself (a “shareholder loan”) or possibly third-party bank or private financing. Generally, the Income Tax Act requires that a loan to a shareholder be repaid within one taxation year after the year in which the loan arose to avoid an inclusion of the borrowed amount in the income of the shareholder. The proposed legislation related to EOT’s will allow for the repayment period to be extended to 15 years to facilitate the repayment of amounts borrowed by the EOT from a qualifying business to fund the acquisition of the shares of the qualifying business.

Even though the rules require that the EOT and the corporation enter into a bona fide repayment arrangement, there is no requirement that the loan ever be repaid. From a practical perspective, this might be helpful if the company falls on hard times and is unable to actually repay the loan – this way the EOT and/or the vendor won’t be “punished” from a tax liability perspective.

Keep in mind that the deemed interest benefit rules under section 80.4 of the Act will apply to these loans and the EOT will be required to include the deemed interest in its income (unless the corporation charges at least the prevailing prescribed rate at the time) with no deduction by the corporation – double tax! If a sufficient rate is charged, it can operate to reduce the income available to distribute to the employee-beneficiaries – also a bad result.

From the vendor’s perspective, a protracted repayment of the purchase price by the EOT will pose a “liquidity mismatch” as the proceeds paid to the vendor may not match the requirement to pay tax on any capital gain realized on the sale of the shares of the qualifying business. Budget 2023 proposes to provide an expanded “capital gain reserve” to the vendor of the shares to allow for an annual inclusion of a minimum of 10% of the gain for each of the successive 10 years following a sale to an EOT.

The EOT will be subject to the legislative provisions that apply to inter-vivos personal trusts in the Income Tax Act. Accordingly, income that is retained in the trust, and not distributed to a qualifying beneficiary of the EOT, will be taxed at the top personal marginal rate applicable in the province of residence of the EOT. All other rules applicable to an inter-vivos personal trust would apply such as (but not limited to):

- Deduction by the EOT for amounts allocated to beneficiaries of the EOT;

- Taxation of allocated amounts in the hands of the beneficiaries;

- T3 Trust Income Tax Return reporting and filing requirements would apply to the EOT;

- The expanded Trust Reporting Rules that will come into effect December 31, 2023, would apply; and,

- Flow through of dividend income character to beneficiaries upon allocation of dividends to beneficiaries of the EOT.

Typically a trust is deemed to dispose of its capital property every 21 years to ensure that a permanent deferral from taxation on accrued gains is not achieved. With the intent of the EOT structure being the continuity and preservation of business ownership by an employee group, this “21-year deemed disposition rule” will not apply for qualifying EOT’s. However, if the trust loses its status as a qualifying EOT, the 21-year rule will be reinstated and the clock will begin ticking until the trust once again meets the EOT conditions. Although the suspension of the 21-year rule can provide administrative and compliance relief, it should be noted that the deferral will, ultimately, come to an end with the potential for a significant income tax liability on a future disposition of the shares of the qualifying business by the EOT. Advance planning by the Trustees must be an ongoing consideration.

The proposed legislative changes presented in the Notice of Ways and Means are detailed and extensive and have a proposed coming-into-force date of January 1, 2024.

Unquestionably, the proposed EOT structure provides an alternative opportunity to owners of Canadian-controlled private corporations when it comes to succession planning. Many owners would much rather see their legacy perpetuated by employees who have a vested interest in the success of the corporation than facilitate a sale that would result in the liquidation or breakup of the company. This can be a valuable alternative when a family succession plan is simply not viable. Caution must be exercised as consideration must be given to the complexity, cost and maintenance of this structure. In the US and the UK, EOT’s have shown to provide substantial benefits to the exiting owner, facilitate succession and feed the desire of employees to exercise their ownership agenda. However, they have also proven to be quite complex, and costly to establish and can also be restrictive. It is also worth pondering the continuity of success of a private enterprise that has been driven by the vision and passion of an entrepreneur that now is turned over to the guidance of either a corporate, professional trustee or an elected Board of Directors who may not share the vision and passion of the entity’s founder.

Notwithstanding their attractiveness, the experience in jurisdictions such as the US and UK has been that often small to mid-size companies find other alternative succession models that are more aligned with their long-term goals. Only time will tell how Canadian businesses will embrace this new succession opportunity.

3. Alternative Minimum Tax

Budget 2023 proposes to change the AMT regime of the Act, which is consistent with the Liberal election platform of 2021, the 2022 Budget, and the Fall Economic Update of 2022. The AMT was introduced in 1986 and has seen little changes since its introduction. Budget 2023 intends to substantially change the method for calculating AMT in an effort to ensure the “wealthiest” Canadians “cannot disproportionately lower their tax bill through advantages in the tax system”…a phrase and concept that is confusing given the Income Tax Act specifically enables taxpayers – rich or poor – to take advantage of various provisions that are provided for.

Budget 2023 indicates that many of the wealthiest Canadians pay little or no personal income tax in a given year. This statement and proposition feels disingenuous as the AMT already exists and essentially ensures that Canadians pay about a 15% tax rate by applying the greater of the AMT and the federal tax otherwise payable. To the extent an individual’s AMT is greater than the tax otherwise payable, the difference can be deducted within the following seven years provided the tax otherwise payable exceeds the AMT amount in the particular year (which is unchanged in Budget 2023).

The proposed changes to the AMT in Budget 2023 are three-fold:

- Broadening the AMT Base by modifying the “adjusted taxable income” calculation for AMT purposes;

- Raising the AMT exemption amount which attempts to provide relief for the so-called “middle class”; and

- Increasing the AMT rate from 15% to 20.5%

No draft legislation has been provided in the Budget documents, however the supplemental notes state that these changes are expected to apply to taxation years beginning after 2023.

Broadening the AMT Base

Budget 2023 proposes to change the amounts and items that are included in “adjusted taxable income” to further limit “tax preferences” such as deductions, credits, and exemptions and thus increasing the amount of income that the AMT is based on. These include:

– Increasing the AMT inclusion rate of capital gains and stock option benefits from 80% to 100% (note that the Budget indicates that gains that are eligible to utilize the lifetime capital gains exemption (“LCGE”) will continue to have a 30% inclusion rate for AMT purposes);

– Capital gains realized upon the donations of publicly listed securities are to be included at 30%, similar to gains sheltered by the LCGE;

– 50% of certain deductions in the determination of net income are disallowed for AMT purposes, including:

- employment expenses, other than those to earn commission income;

- deductions for Canada Pension Plan, Quebec Pension Plan, and Provincial Parental Insurance Plan contributions;

- moving expenses;

- child care expenses;

- disability supports deduction;

- deduction for workers’ compensation payments;

- deduction for social assistance payments;

- deduction for Guaranteed Income Supplement and Allowance payments;

- Canadian armed forces personnel and police deduction;

- interest and carrying charges incurred to earn income from property;

- deduction for limited partnership losses of other years;

- non-capital loss carryovers; and

- Northern residents deductions.

– 50% of most of the currently allowed tax credits that decrease the AMT base are to be disallowed (note the Special Foreign Tax Credit will continue to be allowed in full); and

– No changes to the dividend inclusion and disallowed dividend tax credit (i.e., dividends are included in AMT base without regard to the gross-up and the dividend tax credit continues to be disallowed for AMT purposes).

These changes all increase the amount the AMT is calculated upon, which should result in increased AMT especially where capital gains are realized. It is also interesting to note that some of the deductions that are limited to 50% are aimed at the country’s armed forces and police personnel and limits the deduction for northern residents. These incentives are widely regarded as positive as Canada needs these individuals to keep peace and order and support the economy. As will be noted below, it is expected that the majority of Canadians should not be subject to AMT due to the increase of the AMT exemption amount, however if these specifically targeted individuals begin to earn “tax preferred” income then the benefit of these incentives is reduced.

Raising the AMT Exemption

Budget 2023 proposes to increase the AMT exemption amount (i.e., the amount of “adjusted taxable income” excluded from the AMT calculation) from $40,000 to the lower threshold of the fourth tax bracket (currently $165,431, but expected to rise to ~$173,000 for 2024). This is good news for many Canadians as it effectively carves out the majority of the population from the application of the AMT. However, this increase to the exemption amount does not appear to be enough to offset the other changes to the AMT regime for Canadians who sell their small businesses, farms, or fishing property and who were expecting to be rewarded for the efforts to the Canadian economy by claiming the LCGE (refer to Example 1 below).

Increasing the AMT Rate

Budget 2023 also proposes to increase the AMT rate from 15% to 20.5%. This proposed change indicates that there is belief that a minimum tax of 15% (federally) is not appropriate and that Canadians earning tax preference income should pay more up front. This may be a well intended policy, however there will be situations where individuals who must pay a greater amount of AMT as a result of these changes may not be able to recover their AMT carry forward amount if they lack sufficient income in the subsequent seven years.

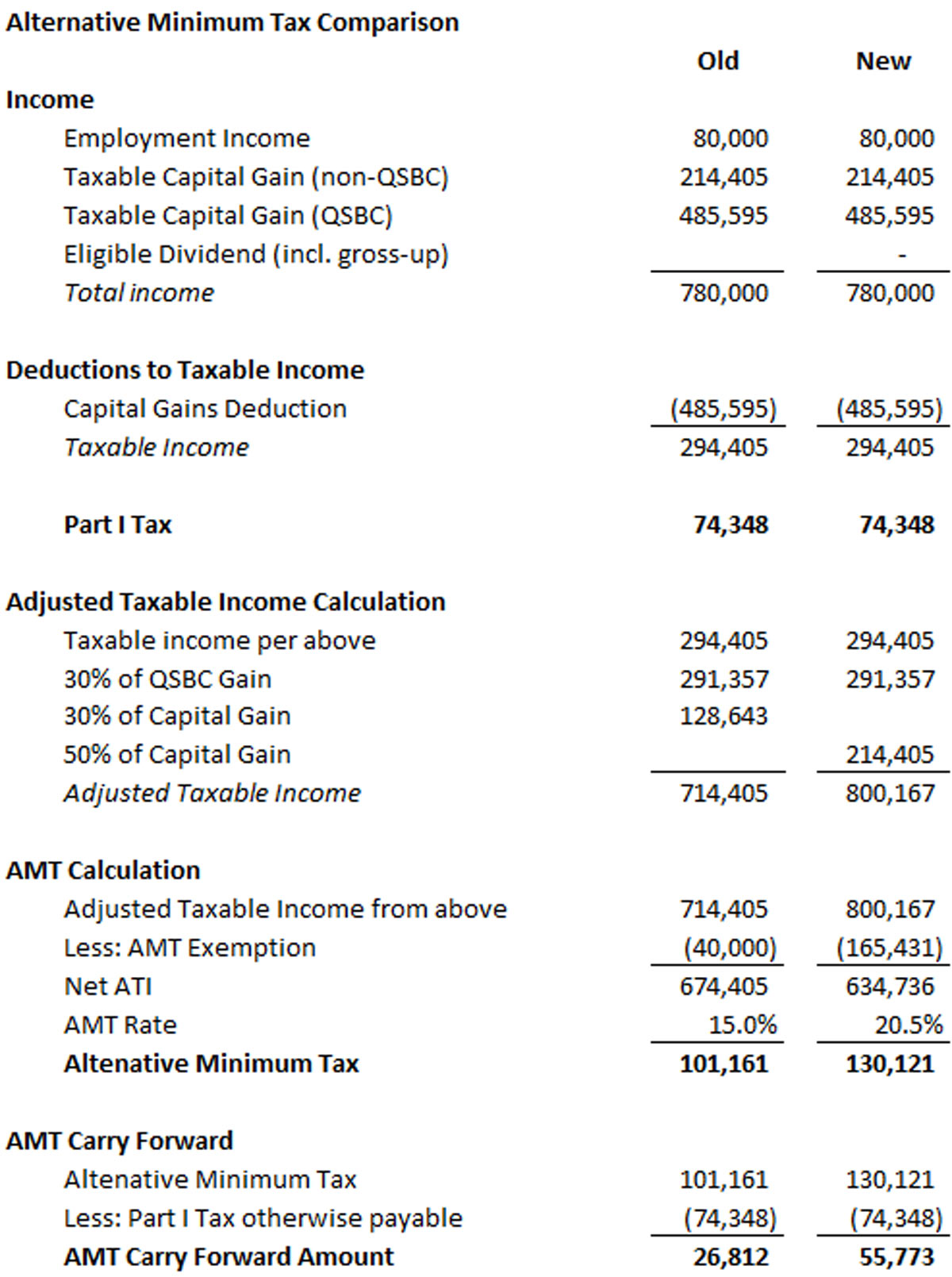

Below are a couple of examples that model out the impact of the proposed changes (note as there was no draft legislation included with the budget for the AMT changes the models below represent our best estimate of the impact of the AMT changes based on the supplemental information provided with the Budget). All examples use 2023 limits and amounts as this information is currently available however the amendments will not be applicable until the 2024 taxation year (for individuals).

Example 1:

This example illustrates the AMT an individual with a modest salary who disposes of qualified small business corporation (“QSBC”) shares with nominal tax cost for $1.4 million.

In this situation the AMT burden has increased significantly. If this individual is retiring and is planning to use the sale proceeds to fund their retirement and is therefore unable to generate sufficient income in their retirement to recover the AMT carry forward amount, then these changes will be more expensive.

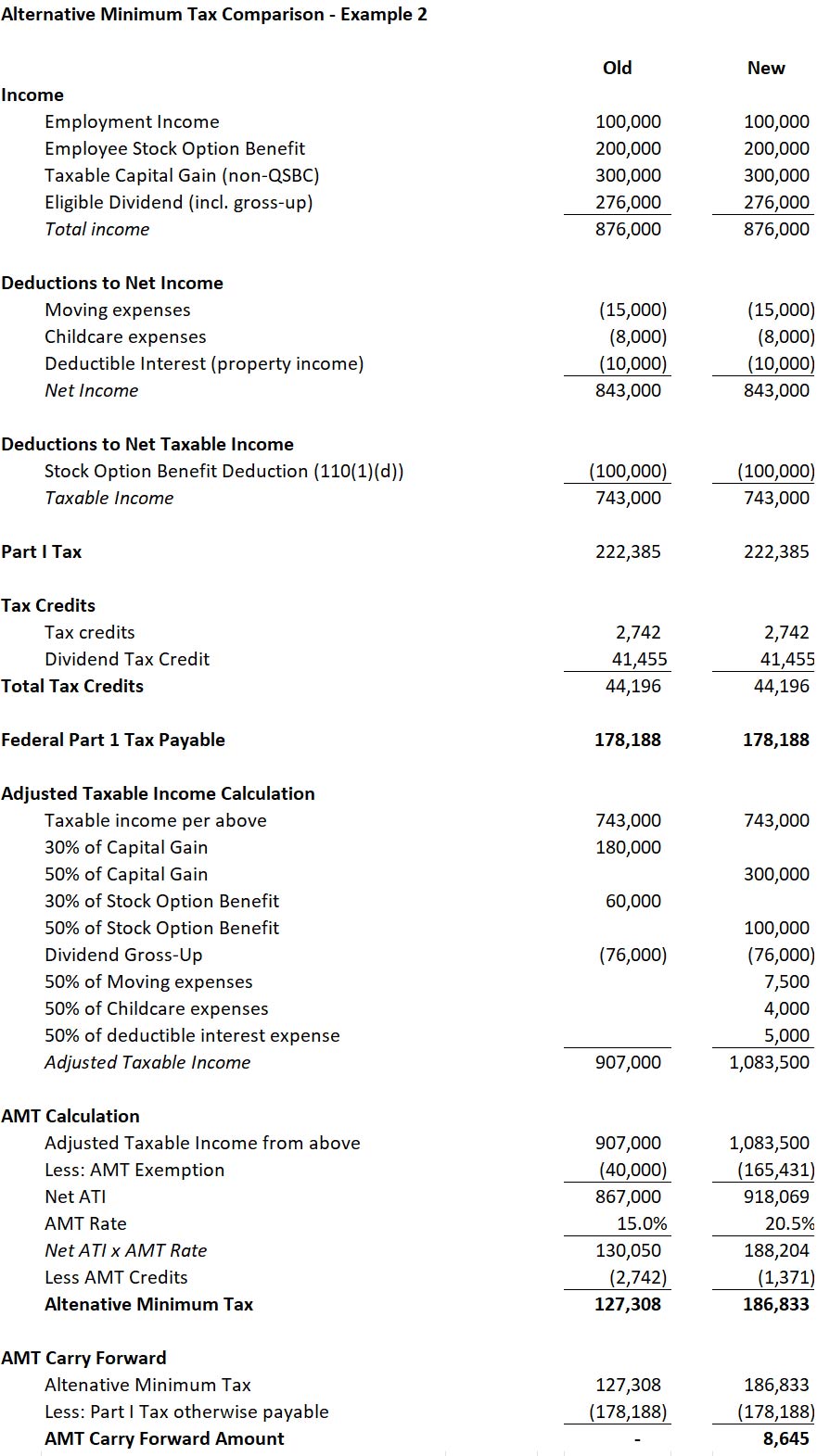

Example 2:

This example is meant to be a more comprehensive illustration of the proposed changes to the AMT calculation and compares the current calculation to the proposed AMT rules.

For accountants, it would be prudent to review and have discussions with your clients to ensure that if the client will be subject to AMT then start planning for additional income to reduce the AMT amount or to recover the AMT in future years. Also, if individuals find themselves in circumstances similar to example 1, perhaps selling LCGE qualifying property in 2023 provides a better tax result than waiting a year or two.

Additionally there are some existing tax planning transactions that may require revisiting, such as:

- heavily leveraged life insurance structures, where an individual taxpayer claims significant amount of interest expense personally to shelter other income;

- planning that relies on large donations of publicly listed securities, including plans that involve donation of publicly listed flow-through shares; and

- paying a spouse just enough to claim childcare expenses.

There are likely many more that should be considered but the above are just a few that immediately come to mind.

4. Changes to the General Anti-Avoidance Rule

Budget 2023 contains major changes to the GAAR including draft legislation to be released for consultation. The consultation period will conclude on May 31, 2023 and the government has indicated that it is interested in gathering stakeholders’ views on the new GAAR proposals. As a quick background, the GAAR was implemented in 1988 to prevent abusive tax avoidance and where the GAAR applies the current legislation denies the tax benefits received that were purportedly unfairly created.

There has been significant discussions by many in government in recent years that the GAAR does not adequately address the issue of abusive tax avoidance. A consultation in August 2022 was conducted where the government identified perceived issues with the GAAR and proposed various ways to address them. As a result, Budget 2023 proposes to “modernize and strengthen” the GAAR by: introducing a preamble; changing the avoidance transaction standard; introducing an economic substance rule; introducing a penalty; and extending the reassessment period in certain circumstances.

The proposed addition of a preamble to the GAAR is couched as addressing interpretive issues. Our view is that the proposed preamble is unnecessary, based on judicial decisions on the GAAR. The government is now expressly adding intention into the legislation, which presumably is intended to further assist in judicial decisions. However, the preamble explicitly states that the GAAR “strikes a balance between” the taxpayer’s need for certainty and the government’s responsibility to protect the tax base. How the courts will interpret striking a balance between these two fundamental objectives will be interesting to say the least. The preamble also includes a provision that states that the GAAR can apply where any “tax strategy” is unforeseen. This will be the first time the term “tax strategy” in included in the Act, inherently resulting in increase interpretive issues, but more importantly it appears that taxpayers can now be subjected to the GAAR even in situations where tax planning played no role in the decision to undertake the transaction, adding more uncertainty to bona fide commercial transactions.

The proposed amendment to the definition of “avoidance transaction” lowers the bar for the application of the GAAR. Currently, the test of avoidance transaction is that a transaction that results in a tax benefit will be considered an avoidance transaction unless it is reasonable to consider that it was undertaken primarily for non-tax purposes. The new draft legislation proposes the test to now be “one of the purposes” can reasonably be considered to obtain a tax benefit, which would significantly expand the scope of what is considered an avoidance transaction. Based on our experience, in many GAAR cases, the finding of an avoidance transaction is often conceded by the taxpayer. We note that this appears at odds with the proposed preamble which purports to that the GAAR can apply in situations where a tax strategy was unforeseen. How can a transaction or series of transactions that is not at all tax motivated (i.e., not an avoidance transaction) have the GAAR applied?

A proposed “economic substance” test is also proposed to be added to the GAAR legislation and will apply at the “misuse or abuse” stage of the GAAR analysis. This addition to the analysis is meant to ensure that economic substance is more robustly considered by the courts. The proposed legislation provides a non-exhaustive list of items that indicate whether a transaction significantly lacks economic substance, that “tend to indicate the transaction results in a misuse or abuse”. The considerations include the opportunity for gain or risk of loss remains unchanged, the tax benefits outweigh the non-tax economic returns, and it is reasonable to conclude that the entire or almost entire purpose of entering into the transactions was to obtain a tax benefit.

The GAAR proposals also include a three-year extension to the normal reassessment period for GAAR assessments by the CRA (unless the transaction is disclosed to the CRA, discussed further below). Apparently the current reassessment periods, generally three or four years, do not provide the CRA with adequate time to review transactions and assess GAAR. This puts a GAAR reassessment window similar to the reassessment period where CRA would assert gross negligence on a taxpayer.

The current impact of the GAAR generally results in placing the taxpayer into the position they otherwise would have been in, meaning the primary punishment is that the taxpayer is subject to the tax they otherwise would have been liable for plus interest on any overdue tax. Budget 2023 proposes to change the assertion that the GAAR is weaker than it ought to be by implementing a penalty equal to 25%(!) of the amount of the tax benefit (excluding tax attribute benefits that may be used subsequently to reduce tax). The penalty, combined with the current higher interest rates, fundamentally changes the calculus as to whether taxpayers will, or should, undertake aggressive tax planning transactions. Aggressive tax planning may no longer be viewed as a cheap source of financing provided by the government.

Interestingly, the draft legislation provided with Budget 2023 provides that no penalty will be assessed where the transaction(s) is / are proactively disclosed to the Minister. Surely this proposal will cause some taxpayers who have received legal advice on their transaction to consider whether or not their privileged advice should be breached so as to avoid the application of the penalty. Not good. Combined with the fact that the legislative proposals do nothing to clarify the uncertainty around whether a transaction or series of transactions is “GAAR”, there is now a punitive penalty that can apply!

The proposed amendments to the GAAR are concerning. Finance surely intends to introduce more clarity into the GAAR, however the proposed legislation appears to introduce new concepts that will increase uncertainty and risk for taxpayers. Ultimately, the game has been changed (or rather, is expected to change) significantly. We will have to wait and see if the consultation period results in changes to the draft legislation. Furthermore, even though Finance has indicated that the date of application will be determined after the May 31, 2023 consultation period has ended, but the effective date of the proposals is unknown. The draft legislation did not provide any insight as to the coming into force date of the legislation. Will Finance assert that these proposals will be effective retroactive to Budget Day?

5. Automatic Tax Filing for Vulnerable Canadians

A welcome announcement in Budget 2023 is the plan to pilot a new automatic tax return filing service for certain vulnerable Canadians who currently do not file tax returns. When implemented, this should help them qualify for benefits which they otherwise would not be able to receive due to the non-filing. At this point, this is still a future project that the Government will be consulting on with stakeholders and community organizations.

Additionally, Budget 2023 mentioned that the CRA will continue to expand their “File My Return” service, and expect to triple the number of Canadians eligible for this service by year 2025.

Again, this is a welcome announcement.

6. Retirement Compensation Arrangements

An RCA is a structure that found significant favour in the late 1990’s and early 2000’s as a means of providing “top hat” retirement benefits to executives of Canadian corporations. The form that the RCA took was generally that of a trust whereby the employer would provide contributions to the trust as deductible benefit funding payments to the trust on behalf of the executive to fund future retirement benefits. These actuarially determined amounts were paid regularly and were also subject to a 50% withholding tax upon contribution to the trust. When the trust undertook to distribute pension benefits to the executive, the RCA would receive a refund of the withholding tax at a rate of $1 for every $2 of benefits paid.

In some instances, employers are either unable to cash-flow contributions to the RCA to satisfy a contractual obligation to the executive, or simply choose not to. In these instances, the employer may elect to settle the retirement obligations to the executive with a “letter of credit” or a “surety bond” which would provide the benefits at the time they become due. To ensure that employers would comply with the withholding requirement, the 50% remittance would be based on the cost to secure or renew the letter of credit or surety bond even though there would be no actual funding of the RCA with actual hard cash. Thus, the corporation had to remit an amount equal to the fee to the CRA AND remit the fee to the financial institution, leaving the 50% remittance stranded, for all intents and purposes.

When the time came for the executive to be paid his/her supplemental retirement benefits, the corporation would meet the requirements directly from corporate revenues as the RCA remained unfunded. The problem, of course, is that the stranded remittances made over the years in respect of the letter of credit or surety bond would never get repaid as there would be no amounts actually distributed from the RCA to trigger the refund.

Budget 2023 fixes the “stranded remittance” condition by removing the requirement for a matching remittance in respect of an RCA withholding under Part XI.3 for fees or premiums paid after March 28, 2023. The proposed amendments also allow for previously remitted amounts in respect of fees or premiums to be refunded to employers based on the supplemental retirement benefits paid out of corporate revenues that were secured by letters of credit or surety bonds.

The Budget provides that this change will apply specifically to retirement benefits paid after 2023.

7. Registered Disability Savings Plans

In Budget 2007, the RDSP was “born” to specifically help alleviate the fiscal demands that people with disabilities and their families face on a daily basis, including disabled adults who may not possess the capacity to enter into the contractual arrangement. They were designed to provide confidence in agency and require the stewardship of the plan by the legal guardian or representative of the disabled beneficiary under the plan. Establishing a legal guardian or representative is not always a simple task and previous Budget measures have provided flexibility by allowing “qualifying family members” to act as the plan owner and steward for incapacitated adults. This was considered a temporary measure that was set to expire on December 31, 2023.

Qualifying family members include a parent, spouse or common-law partner of the disabled adult. Budget 2023 proposes to expand the definition of a “qualifying family member” to include adult (18 years or older) siblings who may now also act to establish and maintain an RDSP on behalf of their incapacitated brother or sister.

Budget 2023 also proposes to extend this proposal beyond 2023 until December 31, 2026.

8. Global Minimum Tax Implementation (OECD BEPS Pillar Two) is Coming to Canada, in 2024, Perhaps?

Like the theme music to the classic horror flick “Jaws”, you can feel the unrelenting and unstoppable coming of the Global Minimum Tax. Budget 2023 again confirms the Canadian government’s intention to implement this in very near future.

As proposed by the Organisation of Economic Co-operation and Development (OECD), there are two prongs to the Global Minimum Tax regime: the Income Inclusion Rule (IIR) and the Undertaxed Profits Rule (UTPR). The IRR is a top-up tax to the ultimate parent entity of a large multinational enterprise (MNE) with respect to income from the MNE’s operations in any jurisdiction where it is taxed at an effective tax rate below 15%. The UTPR is a tax that is imposed on subsidiary operations of a MNE by the subsidiary jurisdiction where the IIR has not been applied to the ultimate parent entity of the MNE by the parent jurisdiction.

Budget 2023 announces Canada’s intention to implement the IIR for fiscal years of MNEs that begin on or after December 31, 2023, and the UTPR for fiscal years of MNEs that begin on or after December 31, 2024. For these purposes, an MNE is considered to have the same fiscal year as its ultimate parent entity.

We think this timeline is an ambitious goal. There are tremendous complexities involved in figuring out a MNE’s effective tax rate as it relates to each jurisdiction it operates in, as well as designing the rules to avoid the many situations that IIR and UTPR could apply unfairly to circumstances that should not be considered mischievous under these rules’ policy intent. However, Finance has had a lot of momentum in terms of introducing great volume of complicated tax legislation in recent years, so, it is possible that the IIR and UTPR will be implemented according to the announced timeline.

It will also be interesting to see where Finance will draw the line in terms of the de minimis threshold for these rules to apply. The Global Minimum Tax as contemplated by the OECD’s BEPS initiative was supposed to target ‘large’ MNEs – those with annual revenues of over 750 million Euros. Will Canada choose a much lower threshold? We are not optimistic on this and we think the de minimis threshold in the Canadian rules will end up much lower than that proposed by OECD. Such would be consistent with Canada’s track record of localizing past OECD initiatives such as the dreaded EIFEL interest limitation rules and the, even-more-dreaded, mandatory disclosure rules.

The coming Global Minimum Tax implementation will be relevant, for example, to any Canadian businesses that may have offshored a portion of their operations to lower-taxed jurisdictions. That said, even if a top-up tax of 15% were to apply, it is still a significantly more preferential rate compared to the combined Canadian federal/provincial general corporate income tax rate, which ranges from 23% to 31% depending on province/territories so it might still be economically sound for these businesses to maintain their offshore structure.

9. Tax on Repurchases of Equity

Budget 2023 provides further details on a new tax on share repurchases by public corporations first announced in the 2022 Fall Economic Statement. This proposed new tax will be imposed on Canadian-resident corporations with publicly listed shares, as well as publicly listed REITS, SIFT trusts and SIFT partnerships (but mutual fund corporations are excluded). The tax will be 2% of the excess of an entity’s equity repurchase over new equity issued from its treasury. If enacted, the proposed tax will apply in respect of equity repurchases that occur on or after January 1, 2024.

10. Registered Education Savings Plan Changes

Budget 2023 tinkers with RESPs so as to increase the amount of withdrawals permitted by the Act and to allow for divorced or separated parents to open joint RESPs. RESPs are tax assisted vehicles aimed to assist Canadians with funding their children’s post-secondary education. The current limit of withdrawals from RESPs are $5,000 for the first 13 weeks of full-time post secondary education and $2,500 for additional 13-week periods or part time study. These limits are increased to $8,000 and $4,000 respectively. The new legislation now permits separated or divorced parents to open a joint RESP to assist in funding children’s education. With the current inflationary environment these changes are positive and should assist students in their education and related expenses.

11. The So-Called “Grocery Rebate”

As the headlines scream “The Government Tackles Affordability With the Grocery Rebate”, realists take the long view that this boutique measure is nothing more than a “drop in the bucket” with little real impact on affordability when it comes to the lower income Canadian’s weekly grocery bill.

The mechanism that will be used to deliver this “tax goodie” is the Goods and Services Tax Credit (GSTC). For eligible individuals and families, Budget 2023 provides an additional GSTC amount as follows:

- $153 per adult;

- $81 per child; and,

- $81 for the single supplement.

The objective is for the Grocery Rebate to be paid as soon as possible following the passage of the legislation and would be phased out immediately as a single payment credit.

As far as “tax goodies” go, this is one of the more laughable that many of us have seen in our taxation careers. The quantum of the credit is certainly far from sufficient to provide any type of relief for a family struggling at or near the poverty line and the overall distribution impact is, in itself, inflationary. If the intent is to put out the fire with gasoline (to quote the great David Bowie) then please stand up and provide your applause to the Government of Canada.

Related Blogs

Why US Tax Season Never Ends When You’re an American Citizen Living Abroad

If you’re a US expat tired of the financial and emotional cost of filing cross-border US taxes,...

Why US Selective Military Service Is Leading Some Expats To Renounce Their US Citizenship.

While millions are glued to their screens for the hit HBO series, a real-life "Succession" drama could...

Want to Avoid Your Own “Succession” Drama? How Renouncing Your US Citizenship Before Death Can Preserve Your Family’s Generational Wealth.

While millions are glued to their screens for the hit HBO series, a real-life "Succession" drama could...